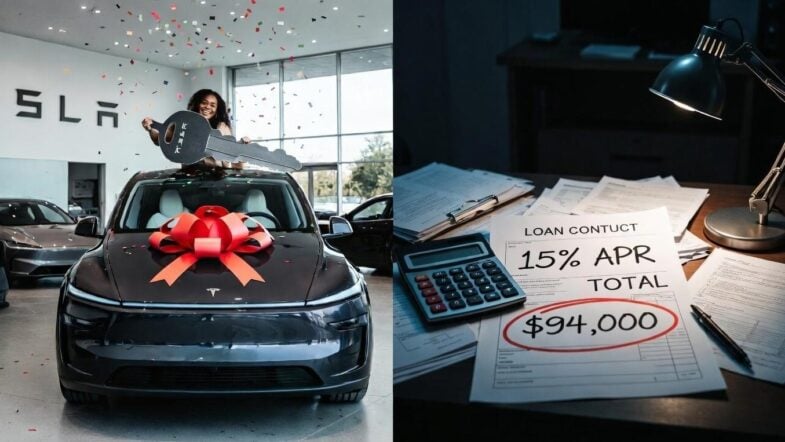

*A viral X video shows a woman celebrating her new Tesla Model Y at a dealership. Her deal? $4,000 down and $1,000 per month. It sounds exciting, but the fine print reveals a financial nightmare: a 15% interest rate stretched over 90 months.

At first glance, driving a new EV feels like a win. In reality, this purchase is a textbook example of how focusing only on the monthly payment—rather than the total cost—leads to disaster. Here is the math, and how to avoid the same expensive mistake.

The Math of a Bad Loan

Based on the terms celebrated in the video, here is what that handshake actually costs:

-

The Car’s Value: A new Tesla Model Y is roughly $40,000–$45,000.

-

The Loan: With only $4,000 down on a $40,000 car, the buyer finances roughly $36,000.

-

The Reality: At 15% APR over 90 months (7.5 years), the total paid for that car balloons to approximately $94,000.

That means paying over $36,000 in pure interest for a vehicle that will depreciate by 10–20% the moment it leaves the lot. In a few years, when the battery warranty expires and replacement costs loom, they will still be stuck paying off a loan on a car worth far less than they owe.

Scroll to continue reading

Why do people fall for this? It usually comes down to the “monthly payment” illusion. Here is how to protect yourself.

A woman is celebrating buying a new car: $4,000 down, $1,000 per month at 15% interest for 90 months ???

— Rain Drops Media (@Raindropsmedia1) March 16, 2026

1. Calculate the Total Cost, Not Just the Payment

Dealers love to ask, “What monthly payment can you afford?” because it distracts from the final price.

-

What to do: Add up the purchase price, taxes, interest over the full loan term, insurance, and depreciation.

-

EV Specifics: Factor in home charging and potential battery degradation. If a $40k car costs you $94k total, you aren’t saving money.

2. Get Pre-Approved First

Walking into a dealership without financing is a mistake.

-

Know the rates: With strong credit, rates hover around 5–7% in early 2026. If a dealer quotes you 15%, you are in subprime territory.

-

Shop around: Credit unions almost always beat dealer financing. Get pre-approved first so you have a bargaining chip.

3. Shorter Terms, Bigger Down Payments

The 90-month loan is a wealth killer.

-

The Risk: You will be “upside down”—owing more than the car is worth—for most of the loan. If the car is totaled, you lose your down payment and have nothing to show for years of payments.

-

The Rule: Aim for 60 months max. Put at least 20% down. Keep total car expenses under 10–15% of your monthly take-home pay.

4. Spot the Red Flags

-

Watch out for: Salespeople who ignore the interest rate and push you to focus only on the monthly payment. “Don’t worry about the rate, can you afford $1,000 a month?” is a classic trap.

-

Add-ons: Be wary of extended warranties rolled into the loan, which you will pay interest on for years.

5. Sleep On It

High-pressure sales stop you from doing the math.

-

The Action: Never sign on the first visit. Take the contract home. If the total cost of a $40,000 car is $94,000, walk away.

The Bottom Line

The woman in the video may be happy today, but that $1,000 payment will feel like a ball and chain for a depreciating asset she can’t afford to sell. Mastering these habits—calculating total cost, securing good rates, and keeping terms short—can save you tens of thousands. If the math doesn’t add up, the celebration won’t last.

(If You Like/Appreciate This EURweb Story, Please SHARE it!)

MORE NEWS ON EURWEB.COM: JeffCars.com’s Review: 2026 Toyota Camry Nightshade AWD2

Don’t Miss Out! Sign up for our Free daily newsletter HERE